Pension Schemes Bill: briefing for Lords Committee stage

This briefing is on behalf of ShareAction, the responsible investment charity.

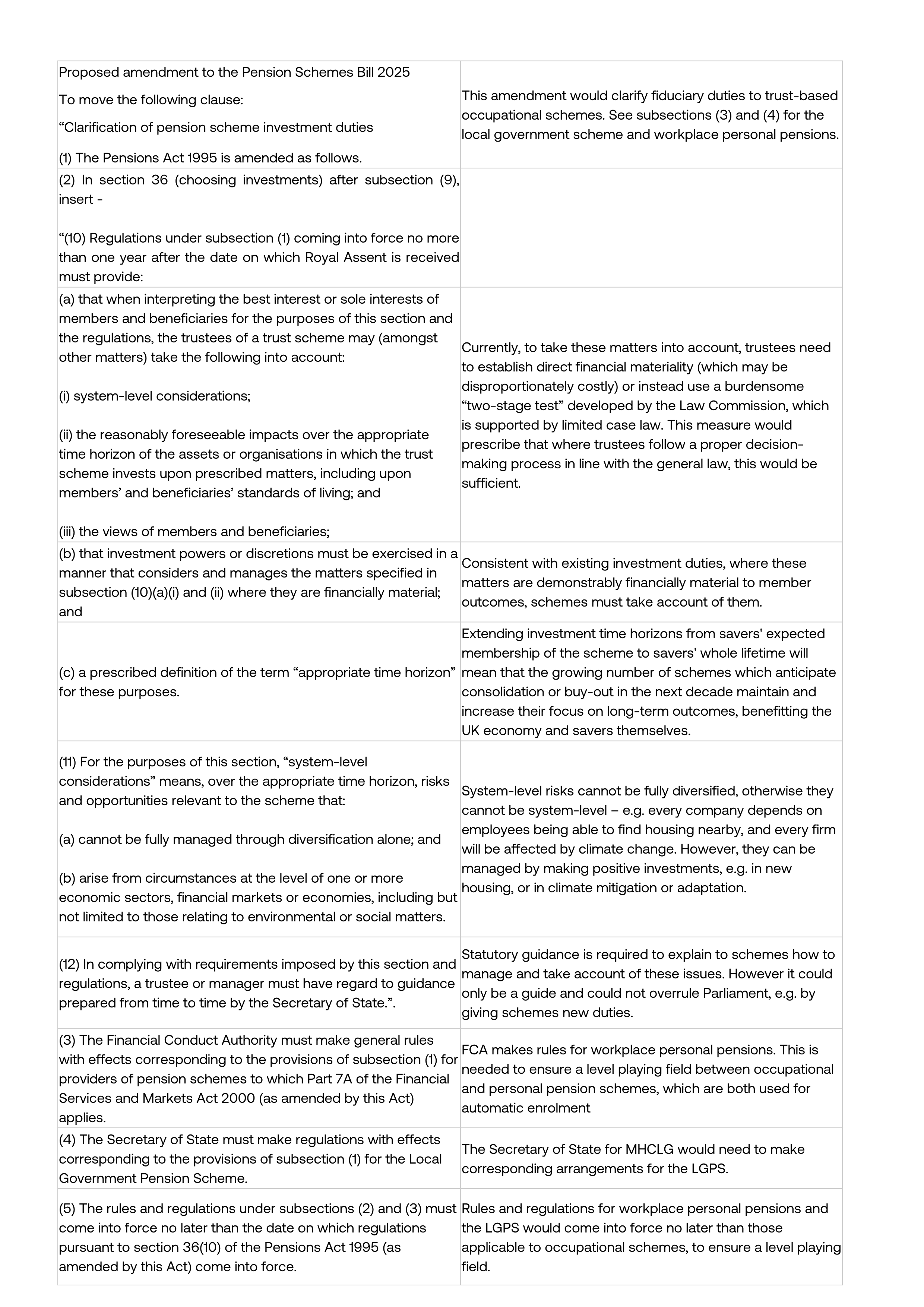

We encourage Peers to speak at Committee debates in support of amendment xxx, which is in the group led by amendment xxx. An annotated copy of the amendment is included in the Annex.

Clarification of pension schemes’ fiduciary duties via amendment xxx would provide the most effective and immediate way of supporting improved outcomes for UK pension savers and boosting investment in UK growth. It would also support investment by pension schemes in housing, decarbonisation, regeneration, education and care – all matters raised by MPs and Peers in earlier debates.

This amendment would reduce the likelihood of needing to invoke Government’s proposed power to set asset allocation targets on pension schemes, which has raised concerns in both Commons and Lords.

The need to clarify fiduciary duty

Fiduciary duties govern how trustees of occupational pension schemes act to fulfill their purpose of providing retirement benefits, but are only briefly covered in statute. Similar provisions apply to the Local Government Pension Scheme (LGPS) and personal pensions. Fiduciary duties are mainly understood through case law, with many key cases centuries-old and others widely misunderstood and misapplied.

The result is that many scheme governance bodies do not feel able to take account of system-level considerations such as the impact on investment returns from climate change and nature loss, housing and infrastructure, health, education, employment or skills. Legal uncertainty also prevents most schemes from taking account of the impacts (positive and negative) of the companies in which they invest on savers’ standard of living – for example, their economic practices or impact on the local community or environment. The law is also unclear on the ability to take account of savers’ views.

Government has recently committed to bring forward guidance, thereby accepting the need for fiduciary duty clarification. But guidance alone will not deliver this in the most comprehensive or effective way, providing the legal certainty that is needed to enable schemes to act. Guidance without a robust legislative framework will also limit parliamentary scrutiny and could be misused by future administrations.

To ensure that pension schemes are voluntarily able to invest productively in members’ interests, including in the UK economy, we encourage Peers to support and speak to amendment xxx which would provide clarification of fiduciary duty in law, rather than via guidance alone.

What Government has said

In the Commons, Government committed to issuing statutory guidance to private sector occupational schemes (but not the LGPS or workplace personal schemes) on their investment duties. To do this, it will bring forward an amendment to give the powers to issue such guidance, most likely at Lords Report stage.

Government has not given a timescale for the guidance itself, and it has previously underdelivered on fiduciary duty clarification. The Sunak administration’s 2023 Green Finance Strategy committed to a series of Government roundtables to understand how it might clarify the law, but none have been convened since the election. The current Government has also publicly welcomed – but not endorsed – the work of the Financial Markets Law Committee (a legal charity) which indicated that schemes should consider broader financial risks like climate change; as well as the NatWest-Cushon/Eversheds opinion on fiduciary duty, which concluded that schemes should take account of savers’ standard of living.

In response to Peers from all parties who spoke in favour of fiduciary clarification at 2nd reading, Ministers sought to argue that introducing “statutory changes to refine investment duties could risk creating rigid and complex obligations, which would reduce the ability of trustees to respond to changing investment landscapes and circumstances.” This is not correct, as we explain on page 3.

Benefits of clarifying fiduciary duty

With new legislative powers, fiduciary duty could be clarified in regulations and statutory guidance in less than 12 months, applying to all pension schemes with immediate effect. This would unlock more UK investment and empower schemes to consider climate, nature, infrastructure, health, skills and standards of living. Legislation would enable a shift in investment decision-making attitudes and practices, whilst ensuring schemes retain complete discretion and control in serving member interests.

The power to manage system-level risks should improve returns by encouraging investments that lift the returns of other companies in which the pension scheme is invested. For example, the success of most UK-based companies will be affected by the extent to which the markets they operate in have healthy, well-educated and -trained populations with adequate housing and good transport infrastructure.

The ability to take account of member standards of living by considering the real-world buying power of their pension - not just its nominal value - would also improve saver outcomes. Savers who retire into a world of high inflation and resource scarcity, where goods such as housing, energy, food or water are more expensive, would experience a worse standard of living than if pension schemes had been clearly permitted in law to take account of living standards and invested to help tackle those risks.

Each measure would support investment in the delivery of UK clean energy, nature protection, home-building, local employment, healthcare and transport infrastructure, as well as investments which make it easier for Government to provide these services by boosting productivity and growth and growing the UK tax base.

The ability to take account of impacts from firms in which schemes invest, and to take account of member views, will also help drive investments that are good for the UK economy.

All of this would be delivered within a continued duty on schemes to act in members’ financial interests. It would not undermine financial returns or remove the existing legal requirement for schemes to “ensure the security, quality, liquidity and profitability of the portfolio as a whole”.

Independent modelling prepared to support this proposal suggests that it has the potential to move over £100bn into UK assets, boosting GDP by 0.3-1.4% by 2029 and reducing emissions by 19 million tonnes a year, similar to the annual emissions of the UK's three largest power stations.

Why statutory guidance alone is not enough

The Pensions Minister indicated at Report stage that “guidance will encapsulate .. wider factors … including what we mean by systemic risks and standards of living” and noted that “there is good support in the industry for providing that clarity”. However Government’s current proposals for guidance risk underachieving for UK savers and UK growth, whilst also doing nothing to boost climate resilience or nature protection.

- The government’s proposal makes no provision for two out of the three main types of workplace pension scheme. The Local Government Pension Scheme, overseen by MHCLG, and workplace personal schemes, overseen by the FCA, are not in scope. Consistency in law across all schemes would ensure all savers benefit. Amendment xx also only applies to a similar subset of schemes.

- Government has offered no timescales for guidance to be produced or come into force. The Lords Science and Technology Committee has flagged the need for ambitious and rapid reforms to encourage a change of thinking by pension schemes, however Government has not progressed roundtables inherited from the Sunak administration or endorsed the Financial Markets Law Committee paper or the Eversheds legal opinion.

- Schemes could not rely on statutory guidance alone in the courts. Statutory guidance without suitable legislative clarification will not give schemes that wish to act the complete confidence to do so. Where the underlying law remains unclear, pension schemes will be exposed to the risk of litigation if they follow statutory guidance as they could still be found in breach of their fiduciary duty. Similarly with amendment xx, schemes will not get the confidence to act from a duty to have regard, if the underlying law is not clear.

- Statutory guidance on its own could be misused by a future Government. Statutory guidance is not reviewed by Parliament. Without a clear legislative framework on pension schemes’ investment duties, a future Government could bring forward guidance without parliamentary scrutiny which sought to subvert pension schemes’ duties to act in savers’ best interests and pressure them into investing in accordance with that Government’s political priorities – for example, discouraging them from investments that were in members’ interests but of which it disapproved, or pressing schemes to provide capital to sectors which that Government did not wish to fund itself.

- Whilst they must have regard to statutory guidance, pension schemes can choose not to follow it and it is virtually impossible to enforce. For example, Government statutory guidance says that pension schemes should produce a plain English summary of their report on how they have managed climate risk; several of the largest schemes have, with no explanation, not produced such a summary, but no compliance action has been taken. Pension schemes could also choose not to follow Government’s proposed statutory guidance on fiduciary duty. There are similar issues with schemes “opting out” in amendment xx.

Statutory guidance can only provide the certainty and stability that schemes need where the legislation governing the investment duties of pension schemes is clear. Confusion, inaction and a lack of oversight will persist until statutory guidance is supported by legislation.

Legislation would not be rigid or complex

ShareAction has published draft regulations on our website which Government is welcome to use. The proposed wording states that schemes may consider system-level issues; the impacts of the organisations in which the scheme invests, including on member standards of living; and members’ views. Schemes must consider and manage system-level considerations and impacts where they are financially material risks, just like any other financially material risk.

The proposed amendment does not prescribe particular actions or targets: it is flexible, allowing schemes to take action appropriate to their size, circumstances and resources. Similarly, the regulations would not specify particular risks which pension schemes must prioritise or disregard; that is for schemes to decide. The proposed legislation is therefore flexible and enabling and would not create ‘rigid and complex’ obligations.

Compliance should not be burdensome. Schemes would simply report their policy in their Statement of Investment Principles – a standard high-level document which is updated every three years. Legal clarity should in fact make investment decision-making more straightforward for schemes and their advisors.

ShareAction is an independent charity and an expert on responsible investment. We work to build a world where the financial system serves our planet and its people. For questions or further information please contact Claire Brinn, ShareAction Senior UK Policy Manager, claire.brinn@shareaction.org

Annotated version of amendment xxx

This amendment has been developed by Stuart O’Brien and Andy Lewis, partners at leading pensions law firm Sackers, working with ShareAction and in consultation with the pensions sector and other key stakeholders.

Explanatory statement

This new clause gives the Secretary of State a duty to make regulations clarifying investment duties of occupational pension schemes, including system-level considerations and other matters including impacts of investee firms, beneficiaries’ standards of living and views. It also imposes duties on the FCA and the Secretary of State to make corresponding rules and regulations for workplace personal pension schemes and the Local Government Pension Scheme respectively.