The climate crisis is the defining issue of our time. The threat is unprecedented in scale and will have far reaching impacts across the globe. The action we take in the next decade will be critical; and the banking sector has a crucial role to play.

On the one hand, banks continue to finance high-carbon activities, undermining global efforts to keep global warming to well-below 2 degree Celsius. They need to stop financing these industries, to avoid the disastrous impacts of climate change for the planet, and their own portfolios. Other the other hand, banks will have a critical role in actively financing the low-carbon transition. Without the banking sector, this transition will be impossible.

It is in this context that we have ranked 20 of the largest European banks, based on their response to the climate crisis.

Only 35% of European banks claim to have Paris-aligned climate strategy

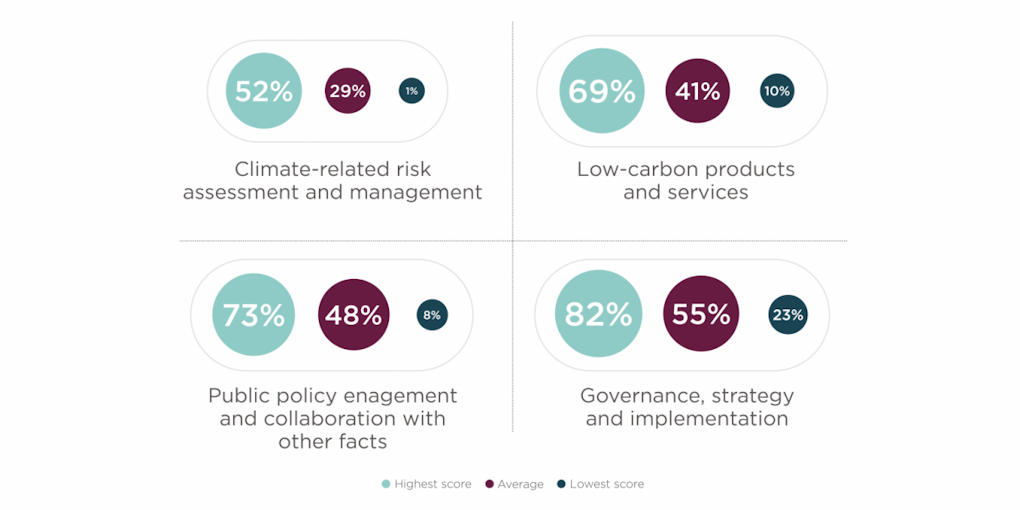

The average score achieved by surveyed banks was just 39.9 per cent, which means on average they are only half way to achieving best practice. In fact not a single bank surveyed has yet reached ‘best practice’ in our ranking – scoring 80 per cent or above, although some banks are showing leading practice in certain areas.

While all banks surveyed publish a strategy on climate change, just 35 per cent of these are aligned with the goals of the Paris Agreement – with just 10 per cent being aligned with its most ambitious goal to hold warming to 1.5 degrees Celsius.

Meanwhile, the governance structure at the surveyed banks remains insufficient to ensure an adequate response to climate change. At 40 per cent of the banks the board still takes a back-seat on climate change, approving the strategy but not taking a driving role, and just 35 per cent of banks set key performance indicators or staff incentives based on climate-related performance.

While current performance remains low, however, we can see that it is possible for banks to drastically improve their climate-related performance in a relatively short time period. Since ShareAction’s first survey of banks in 2017, Lloyds Banking Group has moved from last to second position in the ranking and is a leader in the field.

With time running out to effectively tackle climate change, this finding is reassuring, showing that the banking sector can turn around quickly to play its role in ensuring a successful low-carbon transition.

70 per cent of banks now say they are integrating climate-related risks into traditional types of risk assessment, while some 85 per cent of banks have conducted some form of climate scenario analysis.

However, the range of scenarios used by banks is insufficient. Just 40 per cent are looking at scenarios above 2 degrees Celsius, and even less – 25 per cent – are using below 2 degrees Celsius scenarios. This shows many banks are still failing to take into account the physical risks to their business operations and portfolios from increased warming, or the transition risks associated with ambitious climate action.

Just one bank has carried out a scenario analysis that covers all of its assets.

Banks continue to be exposed to high-carbon assets, with both disclosure and target-setting in this area remaining low – just 60 per cent of banks disclose their exposure to at least one high-carbon asset. Transparency in this area is vital for investors and stakeholders to be able to assess both how at risk a bank is from a rapid low-carbon transition, and how much it is contributing to the problem.

Most banks (80 per cent) now have a policy in place to prohibit coal-related project finance – i.e. for coal mines and power stations – but just 55 per cent restrict finance for new clients reliant on coal mining or power, and just 15 per cent exclude existing existing clients.

Not a single bank has a phase-out target for oil and gas financing although some do have policies in place for unconventional forms of these fuels, such as Arctic drilling or tar sands. Again, the focus of these policies is on project financing (65 per cent of banks) rather than general corporate financing for those companies heavily engaged in unconventional oil and gas (just 35 per).

Just 30 per cent of banks currently disclose a breakdown of their financed power generation portfolio. Of those that do, renewables currently makes up an average 37 per cent – with around 40 per cent of banks’ financed power generation portfolio still in fossil fuels.

However, banks are actively looking to scale up green financing and develop a range of green products and services, including green mortgages and bonds.

70 per cent of surveyed banks are publicly disclosing targets to increase green financing, while 70 per cent also have dedicated staff in each major division – i.e. retail banking, commercial banking etc – focused on developing new products and services. This is encouraging given the critical role of banks in mobilising capital to finance the low-carbon transition.

However, there is still a lot of variation in just what constitutes green financing or a green product and service, making comparison between banks difficult. Banks themselves report a lack of standardisation as a key barrier to scaling up green financing. Other barriers also remain, including transaction costs, lack of data and project pipelines.

Overall, much work remains to be done to raise the standard of banks’ response to the climate change. While some banks demonstrate leadership in certain areas, none perform strongly across all topics. The scale and urgency of the challenge ahead demands much more than ‘business-as-usual’. But we have seen how quickly banks can scale up their ambition, and we encourage all banks to take urgent steps to increase ambition.